Rising Management Risks Driven by External Factors

In the fiscal year ended March 31, 2026, external uncertainties intensified, with tariff-related issues emerging at the beginning of the fiscal year in April, followed by heightened geopolitical risks after the turn of the year. These factors significantly impacted the global economy and, through channels such as crude oil and financial market prices, materially influenced capital investment demand, which is a key driver of our business performance.

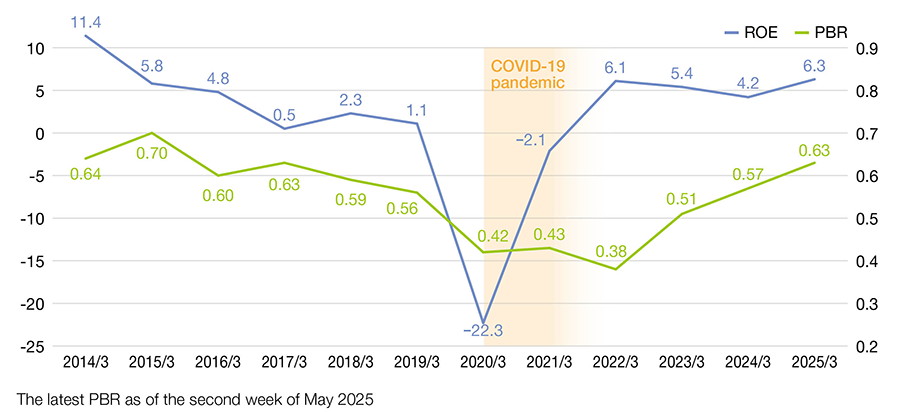

Our price-to-book ratio (PBR) temporarily exceeded 0.8x; however, upward momentum in our share price was constrained due to financial market volatility. Regardless of the operating environment, we remain committed to achieving our target PBR of 1.0x by steadily advancing a range of initiatives.

Our Business Strategy

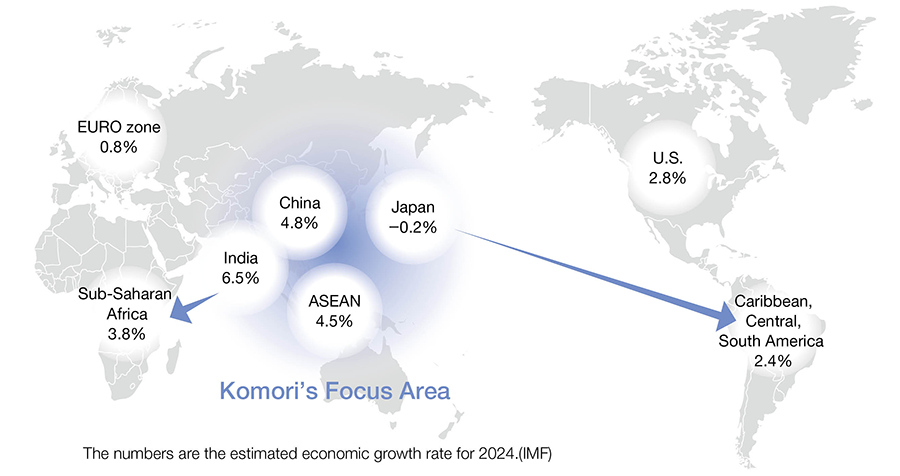

The fiscal year ending March 2027 marks the final year of our 7th Medium-Term Management Plan. Our core business strategy remains unchanged. In our foundational offset printing business, we aim to further expand our top market share in Southeast Asia, India, and South Asia—regions that continue to demonstrate the strongest economic growth globally.

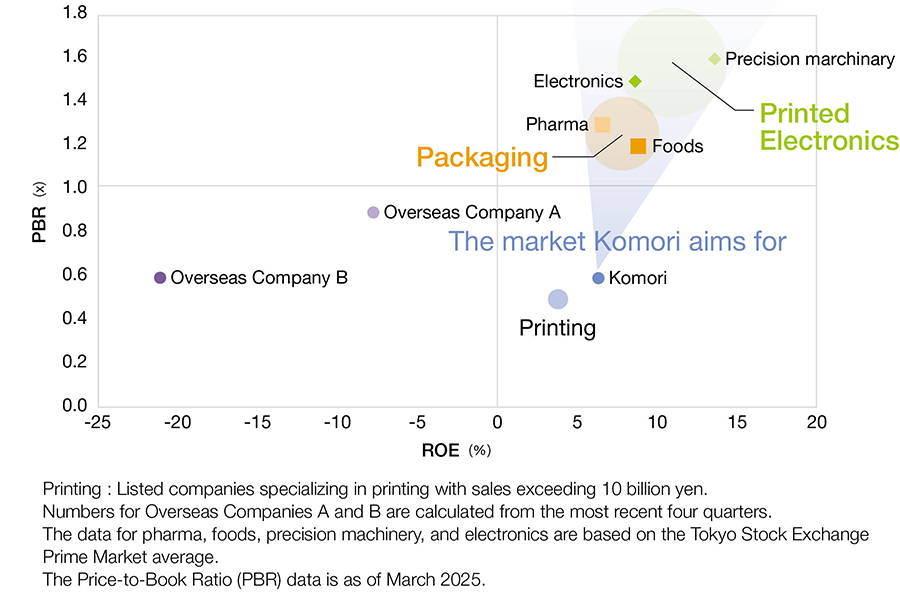

At the same time, we are shifting our overall business portfolio toward higher-growth areas, including packaging and semiconductor-related fields. By firmly achieving the KPIs set forth in our medium-term plan—an operating margin of 7% and ROE of 6%—we aim to build a resilient earnings structure capable of withstanding external risks.

Improving Profitability

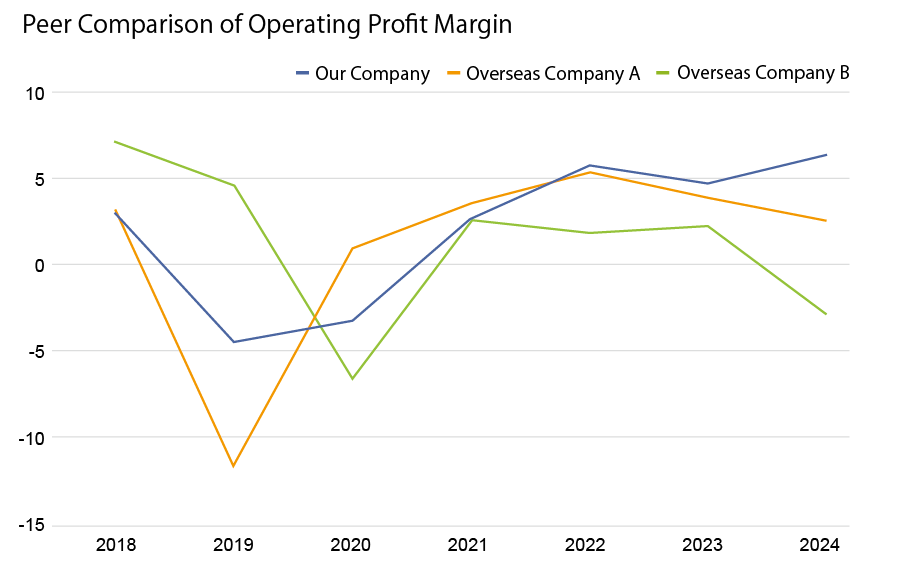

As an export-oriented company, we benefit from yen depreciation, and it is important to carefully assess the impact of foreign exchange fluctuations on our financial performance. On a U.S. dollar basis, our performance has not improved to the same extent as observed in yen terms since the COVID-19 pandemic (net sales: ¥90.2 billion in FY March 2019 vs. ¥111.1 billion in FY March 2024; USD 813 million vs. USD 743 million).

Nevertheless, our profitability has improved at a pace exceeding that of our overseas peers. This is largely attributable to our integrated production system at our core Tsukuba Plant, which emphasizes cost efficiency and is unmatched by competitors. Strong demand in Asia has also supported this improvement in performance.

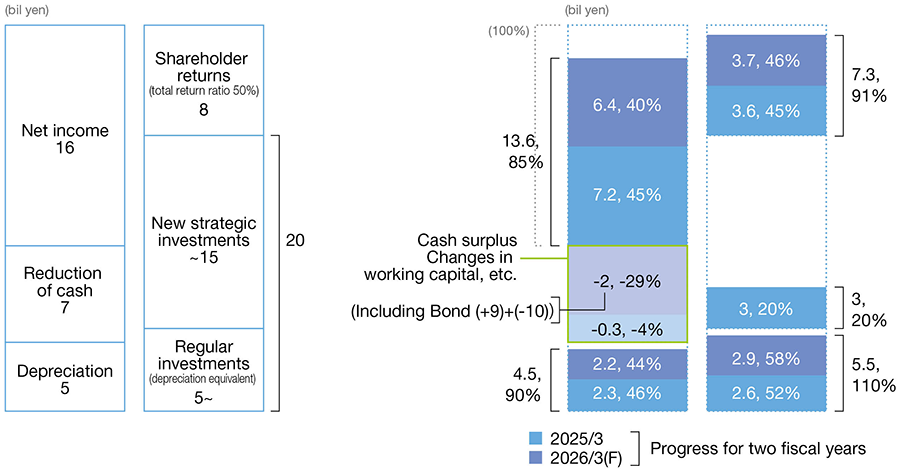

Capital Allocation

Progress under the current medium-term plan has been solid. Cash inflows, including profits and depreciation, have generally exceeded initial assumptions, while cash outflows—such as maintenance and renewal capital expenditures and shareholder returns—have also surpassed targets.

On the other hand, new strategic investments have fallen short by approximately ¥5 billion. While we continue to actively pursue such investments, if there remains a shortfall versus the planned level, we intend to return capital to shareholders through measures such as enhanced shareholder returns.

Looking ahead to the 8th Medium-Term Management Plan, we will further strengthen these initiatives with the aim of achieving ROE that exceeds our estimated cost of capital of 8–9%.

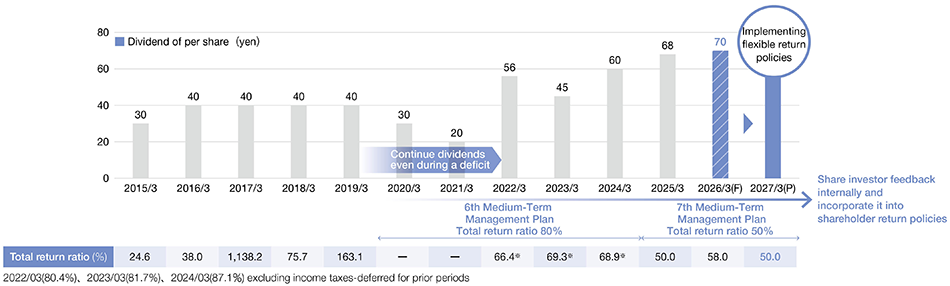

Dividend Policy

For the fiscal year ending March 2027, we plan to pay an annual dividend of ¥75 per share, consisting of an interim dividend of ¥35 and a year-end dividend of ¥40. This corresponds to a total payout ratio of approximately 55% based on our earnings forecast.

We will maintain a flexible approach going forward, taking into account business performance, financial conditions, and investor expectations.

May 2026